Derived Indicators

Given a base indicator, usually coming from the literature, a whole set of indicators is derived from it and made available to you. Here are described the derived indicators.

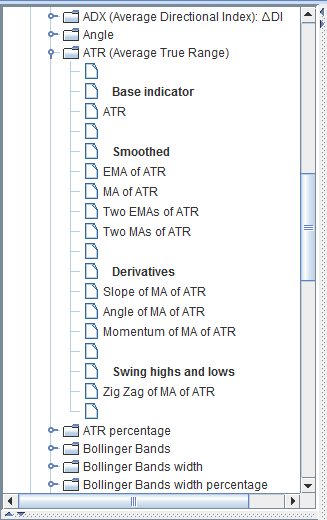

In the previous picture, the ATR is the base indicator. All other indicators in the ATR branch are derived indicators.

Function Composition

Derived indicators are built through function composition, by applying one indicator to the output of another:derived = third (second (first (price) ))

Data Input of Indicator Composition

The data input of the first indicator of the chain is always the price. The data input of the second indicator in the chain is the output of the first indicator. And so on.Formulae Section in the User Interface

Note that in theFormulae section of the base indicator appearing in the description pane of the Graphical User Interface,

the data input is always the price, because that's what happens for the base indicator.

But the same formulae hold substituting the price with any other sequence of values; it is just a name of a variable.

Output Bounds Section in the User Interface

As a corollary to the previous point, theOutput bounds section of the base indicator in the User Interface

reports the bounds when the base indicator is applied to prices, which are always positive numbers.

But the bounds of the function, per se, could be different.

For instance, the Rate of Change (ROC) per se is unbound but, when applied to a positive quantity, its lower bound is -100.

Input Parameters Order

In the input parameters list, the parameters of the last applied indicator appear first, and the parameters of the first applied indicator appear last. Example:parameter 1 of third parameter 2 of third parameter 1 of second parameter 1 of first parameter 2 of first parameter 3 of first